How to Read a Paystub: The Complete Guide to Every Section, Every Tax, and Every Line

Most people receive a paystub every week or two for their entire working lives — yet a surprising number have never had anyone explain what every single line actually means. You know the big number at the top (gross pay) and the disappointing number at the bottom (net pay). But everything in between? That's where most people's eyes glaze over.

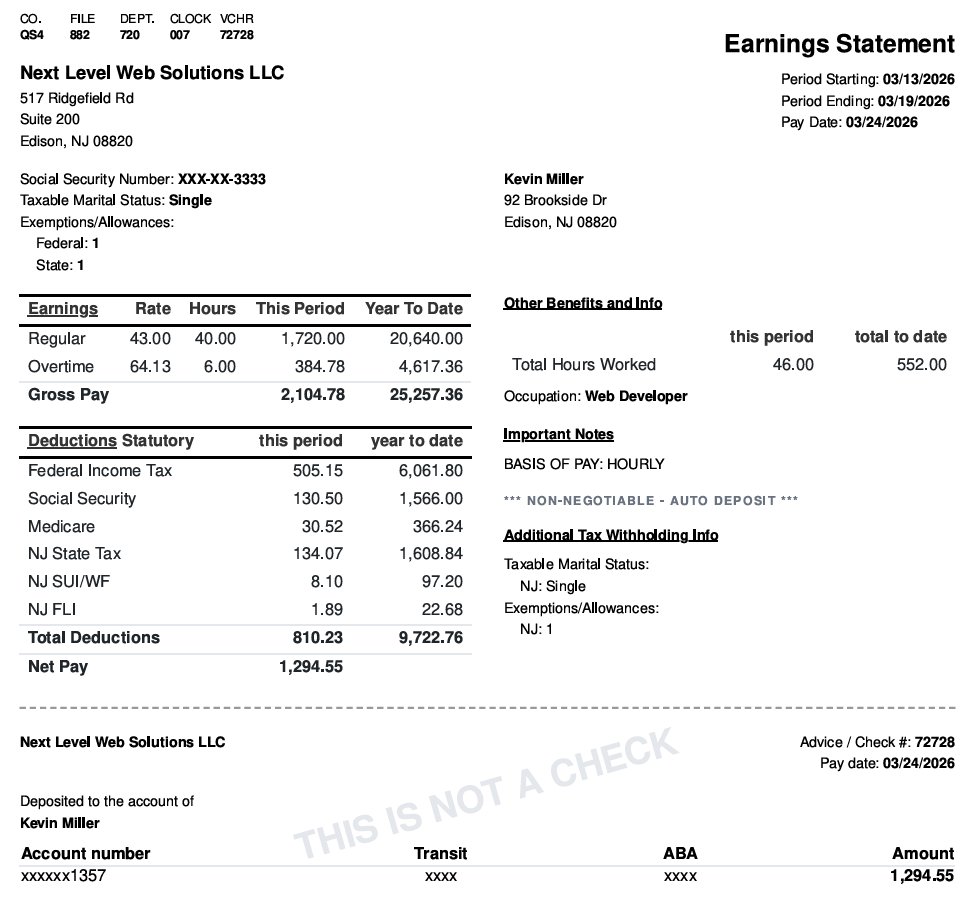

This guide changes that. We'll walk through every section of a real paystub — using Kevin Miller's actual earnings statement from Next Level Web Solutions LLC as our example — and explain exactly what each field means, how the numbers are calculated, why that information matters, and what to do if something looks wrong.

Whether you're a W-2 employee reading your first paystub, a self-employed worker trying to create one for a loan application, a small business owner issuing paystubs to employees, or a student learning about personal finance — this guide has everything you need.

- What is a paystub?

- Interactive paystub — click every section

- Employer information section explained

- Employee information section explained

- Pay period, pay date, and pay frequency

- Earnings: regular pay, overtime, and more

- Gross pay vs. net pay — the critical difference

- Federal income tax withholding explained

- FICA taxes: Social Security and Medicare

- State income tax — all 50 states listed

- Other deductions: 401k, health insurance, HSA, and more

- Year-to-date (YTD) totals explained

- Direct deposit and payment confirmation

- Pay frequency: weekly, bi-weekly, semi-monthly, monthly

- How to spot errors on your paystub

- Self-employed paystubs: how to create your own

- Using your paystub for income verification

- Complete paystub glossary — 40+ terms defined

- Frequently asked questions

What Is a Paystub?

A paystub — also called a pay slip, paycheck stub, earnings statement, or check stub — is a document that accompanies each paycheck or direct deposit and provides a detailed breakdown of an employee's earnings for a specific pay period. It shows how much was earned, how much was withheld in taxes, what other deductions were taken, and what the employee actually received.

Paystubs serve multiple purposes beyond simply showing how much you got paid:

- Income verification — Landlords, lenders, and banks use paystubs to verify your income when you apply for an apartment, car loan, mortgage, or personal loan

- Tax filing — Your year-end W-2 should match your final paystub's YTD totals; discrepancies signal a payroll error

- Payroll auditing — Paystubs let both employers and employees verify that pay calculations are correct

- Benefits tracking — Paystubs document retirement contributions, health insurance premiums, and other benefit deductions

- Legal protection — In disputes over wages or hours, paystubs serve as documented evidence

- Financial planning — Understanding your paystub helps you manage cash flow and understand your true tax burden

Interactive Paystub Walkthrough

Below is Kevin Miller's real paystub. Click or tap any numbered zone — or use the color-coded legend buttons — to see a detailed explanation of that section.

Employer Information Section — Explained in Full

The top-left block of every paystub identifies the company that issued it. On Kevin's paystub this is Next Level Web Solutions LLC, 517 Ridgefield Rd, Suite 200, Edison, NJ 08820.

What the employer section contains

- Company legal name — The registered business name, which should match the name on W-2 forms and tax filings

- Business address — The official address of record, which lenders may use to verify employment

- Internal codes — CO. FILE (company file number), DEPT. (department code), CLOCK (employee clock number), VCHR (voucher/check number). These are payroll system identifiers used for internal tracking and audit trails

- EIN (sometimes shown) — The Employer Identification Number, a federal tax ID assigned by the IRS. Not always shown on paystubs but may be included

Employee Information Section — Explained in Full

The employee section identifies the person receiving payment and their tax filing parameters. Getting this section right is critical — it directly determines how much federal and state income tax is withheld from every paycheck.

Employee section fields

- Full legal name — Must match the name on file with the IRS and Social Security Administration

- Home address — Used to determine state and local tax obligations

- Social Security Number (masked) — Shown as XXX-XX-XXXX with only the last 4 digits visible for security. Used by the IRS to match earnings records

- Taxable Marital Status — From the employee's W-4 form. Options are Single, Married Filing Jointly, Married Filing Separately, Head of Household, or Qualifying Surviving Spouse

- Exemptions/Allowances — From the employee's W-4. Each allowance reduces the amount withheld per period. The 2020 W-4 redesign eliminated allowances for new employees and replaced them with dollar amounts, but many employers still use the old system for existing employees

- Occupation — Job title or classification, used for workforce reporting and sometimes for insurance or workers' compensation purposes

How marital status affects withholding

This is one of the most misunderstood aspects of paystub reading. Kevin is listed as Single with 1 allowance. Here's how different filing statuses affect withholding on the same $2,104.78 gross pay:

| Filing Status | Approx. Federal Tax Withheld | Difference vs. Kevin | Why |

|---|---|---|---|

| Single, 0 allowances | ~$545 | +$40 more | Maximum withholding, no allowances claimed |

| Single, 1 allowance (Kevin) | $505.15 | — | Standard single filer with one personal allowance |

| Married Filing Jointly, 2 allowances | ~$280 | −$225 less | Lower married brackets, multiple allowances |

| Head of Household, 1 allowance | ~$420 | −$85 less | More favorable brackets than Single |

| Exempt (claimed exempt) | $0 | −$505 less | No withholding — full tax due at filing time |

Pay Period and Pay Date — What Every Date Means

Every paystub contains at least two dates — and confusing them is a very common mistake.

- Period Starting / Period Ending — The first and last days of the work period this paystub covers. On Kevin's stub: March 13–19, 2026. This is when the work was performed.

- Pay Date — The date the payment was actually issued and deposited. On Kevin's stub: March 24, 2026 — five days after the period ended. This is when the money arrived.

The gap between the period end date and the pay date is called the payroll processing lag. It exists because employers need time to compile hours, calculate taxes, process deductions, submit the payroll file to their bank, and allow the ACH transfer to clear. The typical lag is 3–7 business days.

Earnings: Regular Pay, Overtime, and Every Pay Type Explained

The earnings section is the heart of the paystub. It shows every type of compensation earned during the pay period, broken down by type, rate, hours, and amount.

Regular Pay

Regular pay is compensation earned for standard scheduled hours at the employee's base rate. Kevin earns $43.00/hour for 40 regular hours = $1,720.00 this period.

For salaried employees, regular pay is a fixed amount per period regardless of hours worked. A salaried employee earning $80,000/year paid bi-weekly receives exactly $3,076.92 per period, every period, whether they worked 35 hours or 55 hours that week.

Overtime Pay

Under the Fair Labor Standards Act (FLSA), non-exempt employees must be paid at least 1.5× their regular rate for all hours worked beyond 40 in a workweek. Kevin worked 6 overtime hours at $64.13/hour (43.00 × 1.5 = $64.50 — the slight variance is due to NJ overtime rounding rules) = $384.78.

Other earnings types you may see on a paystub

| Earnings Type | What It Means | Tax Treatment |

|---|---|---|

| Regular / Base Pay | Standard hours at base rate | Fully taxable |

| Overtime (OT) | Hours over 40/week at 1.5× rate | Fully taxable |

| Double Time | Hours at 2× rate (holidays, some states) | Fully taxable |

| Bonus | Performance, signing, or holiday bonus | Taxable; often withheld at 22% supplemental rate |

| Commission | Percentage of sales generated | Fully taxable; may use supplemental withholding |

| Vacation Pay / PTO | Paid time off used during the period | Fully taxable |

| Sick Pay | Paid sick leave used during the period | Fully taxable |

| Tips | Reported tip income (restaurant/hospitality) | Fully taxable; must be reported and withheld |

| Severance | Pay upon termination of employment | Fully taxable; often 22% supplemental rate |

| Reimbursements | Business expense repayments (mileage, etc.) | Not taxable if under accountable plan |

| Imputed Income | Value of non-cash benefits (e.g., group life over $50k) | Taxable; added to gross for tax calculation only |

| Shift Differential | Extra pay for evening, night, or weekend shifts | Fully taxable |

| Hazard Pay | Additional pay for dangerous working conditions | Fully taxable |

Gross Pay vs. Net Pay — The Most Important Distinction on Any Paystub

If you understand nothing else about a paystub, understand this: gross pay and net pay are very different numbers, and confusing them has real financial consequences.

Gross pay is the total amount you earned before any taxes or deductions are applied. It's the number on your job offer letter, the number your employer reports to the IRS, and the number lenders and landlords use to qualify you for loans and rentals. Kevin's gross pay this period is $2,104.78.

Net pay is what actually arrives in your bank account after all withholdings. Kevin's net pay is $1,294.55 — about 61.5% of his gross pay. The remaining 38.5% ($810.23) went to federal and state taxes and other statutory deductions.

The gross-to-net calculation on Kevin's paystub

| Item | Amount | % of Gross |

|---|---|---|

| Gross Pay | $2,104.78 | 100% |

| Federal Income Tax | −$505.15 | 24.0% |

| Social Security | −$130.50 | 6.2% |

| Medicare | −$30.52 | 1.45% |

| NJ State Tax | −$134.07 | 6.4% |

| NJ SUI/WF | −$8.10 | 0.38% |

| NJ FLI | −$1.89 | 0.09% |

| Net Pay | $1,294.55 | 61.5% |

Need to Create a Professional Paystub?

PaystubASAP generates accurate paystubs in under 2 minutes — with all sections above automatically calculated including correct gross pay, all tax withholdings, YTD totals, and net pay. Works for employers, employees, freelancers, and contractors.

Create My Paystub Now →100% accurate 2026 tax calculations for all 50 states · Instant PDF · Trusted by 50,000+ users

Federal Income Tax Withholding — Fully Explained

Federal income tax is the largest single deduction on most paystubs. It funds the federal government — defense, Social Security, Medicare, federal highways, and hundreds of other programs. Unlike FICA taxes (which are flat-rate), federal income tax is progressive — meaning the more you earn, the higher percentage you pay on income above each bracket threshold.

2026 Federal Income Tax Brackets

| Rate | Single Filers | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 10% | $0 – $11,925 | $0 – $23,850 | $0 – $17,000 |

| 12% | $11,926 – $48,475 | $23,851 – $96,950 | $17,001 – $64,850 |

| 22% | $48,476 – $103,350 | $96,951 – $206,700 | $64,851 – $103,350 |

| 24% | $103,351 – $197,300 | $206,701 – $394,600 | $103,351 – $197,300 |

| 32% | $197,301 – $250,525 | $394,601 – $501,050 | $197,301 – $250,500 |

| 35% | $250,526 – $626,350 | $501,051 – $751,600 | $250,501 – $626,350 |

| 37% | Over $626,350 | Over $751,600 | Over $626,350 |

How payroll calculates federal withholding per paycheck

Payroll systems don't simply divide your annual tax bill by your number of pay periods. Instead, they use the IRS Publication 15-T withholding tables, which effectively annualize each paycheck to estimate annual income, calculate the annual tax liability at that level, then divide by pay periods. This is why:

- A week with overtime may have disproportionately high withholding (the annualized income estimate is higher)

- A bonus or commission payment is often withheld at the flat 22% supplemental rate rather than your normal effective rate

- People with irregular income may find their withholding doesn't match their actual annual tax liability

The standard deduction's effect on withholding

The 2026 standard deduction is $15,000 for single filers and $30,000 for married filing jointly. Your W-4 withholding calculation already accounts for the standard deduction, which is why your effective withholding rate appears lower than your marginal tax bracket rate.

FICA Taxes: Social Security and Medicare Fully Explained

FICA stands for the Federal Insurance Contributions Act. It's the law that mandates withholding for Social Security and Medicare — the two federal programs that provide retirement income, disability benefits, and healthcare coverage for Americans 65 and older.

Unlike income tax, FICA is a flat-rate tax — everyone pays the same percentage regardless of income level (up to the wage base for Social Security).

Social Security Tax

- Rate: 6.2% of gross wages (employee share)

- Employer match: 6.2% (employer pays an identical amount on top — this never appears on your paystub)

- 2026 wage base: $176,100 — once your YTD earnings exceed this, Social Security withholding stops for the rest of the year

- Kevin's amount: $2,104.78 × 6.2% = $130.50

- What it funds: Retirement benefits, disability insurance (SSDI), survivor benefits for dependents of deceased workers

Medicare Tax

- Rate: 1.45% of all gross wages (no wage base cap)

- Employer match: 1.45%

- Additional Medicare Tax: 0.9% on wages above $200,000 for single filers ($250,000 for married filing jointly) — employer does not match this portion

- Kevin's amount: $2,104.78 × 1.45% = $30.52

- What it funds: Hospital insurance (Medicare Part A) for Americans 65+ and eligible disabled individuals

Total FICA burden: employee vs. self-employed

| Tax | Employee Pays | Employer Pays | Self-Employed Pays | Notes |

|---|---|---|---|---|

| Social Security | 6.2% | 6.2% | 12.4% | Up to $176,100 wage base (2026) |

| Medicare | 1.45% | 1.45% | 2.9% | No wage base limit |

| Additional Medicare | 0.9% | None | 0.9% | On income over $200K (single) |

| Total FICA | 7.65% | 7.65% | 15.3% | SE gets 50% deduction on Schedule SE |

State Income Tax on Your Paystub — Complete 50-State Reference

Kevin's paystub shows an NJ State Tax deduction of $134.07. But not every state has a state income tax — and for those that do, rates and structures vary enormously. If you live in a no-tax state, that line simply won't appear on your paystub. If you live in California at a high income level, your state tax line could rival your federal tax line.

- Alaska — No income tax and no sales tax; state funded largely by oil revenues

- Florida — No income tax; funded by sales tax and tourism revenue

- Nevada — No income tax; funded by gaming and hospitality taxes

- New Hampshire — No tax on wages; a tax on interest and dividends was fully phased out in 2025

- South Dakota — No income tax; funded by sales tax and tourism

- Tennessee — No income tax on wages as of 2021; the Hall Tax on investment income was eliminated

- Texas — No income tax; constitutionally prohibited; funded by property and sales taxes

- Washington — No income tax on wages; a capital gains tax applies to gains over $262,000 but not to ordinary wages

- Wyoming — No income tax; funded largely by mineral extraction revenues

Complete 50-State Income Tax Reference

| State | Structure | Rate(s) (2026) | Notes |

|---|---|---|---|

| Alabama | Graduated | 2% – 5% | 3 brackets; top rate on income over $3,000 for single filers |

| Alaska NO TAX | None | 0% | No income or sales tax; oil revenue funded |

| Arizona | Flat | 2.5% | Flat rate since 2023; significant reduction from prior graduated system |

| Arkansas | Graduated | 2% – 4.4% | Top rate reduced from 5.9% in recent years; further cuts planned |

| California | Graduated | 1% – 13.3% | Highest top rate in the US; 1% Mental Health Services Tax on income over $1M; 10 brackets |

| Colorado | Flat | 4.4% | Flat rate; TABOR refunds can reduce effective rate in surplus years |

| Connecticut | Graduated | 2% – 6.99% | 7 brackets; phase-out of low-income exemptions at higher incomes |

| Delaware | Graduated | 0% – 6.6% | 6 brackets; top rate on income over $60,000 |

| Florida NO TAX | None | 0% | No income tax; constitutionally prohibited |

| Georgia | Flat | 5.49% | Transitioning to flat; scheduled to reduce toward 4.99% by 2029 |

| Hawaii | Graduated | 1.4% – 11% | 12 brackets; second-highest top rate in the US; top rate on income over $400K |

| Idaho | Flat | 5.8% | Flat rate since 2023; prior graduated system had rates up to 6% |

| Illinois | Flat | 4.95% | Constitutionally required to be flat; no graduated tax allowed without amendment |

| Indiana | Flat | 3.05% | Flat state rate; all 92 counties additionally impose county income taxes ranging 0.5%–2.9% |

| Iowa | Flat | 3.8% | Transitioning to flat rate; reducing toward 3.5% by 2026 |

| Kansas | Graduated | 3.1% – 5.7% | 3 brackets; top rate on income over $30,000 for single filers |

| Kentucky | Flat | 4% | Flat rate reduced from 4.5% in 2024; targeting further reductions |

| Louisiana | Graduated | 1.85% – 4.25% | 3 brackets; significant rate reductions effective 2025 |

| Maine | Graduated | 5.8% – 7.15% | 3 brackets; top rate on income over $58,050 for single filers |

| Maryland | Graduated | 2% – 5.75% | 8 brackets; all 23 counties plus Baltimore City add local income tax (2.25%–3.2%) |

| Massachusetts | Flat + Surtax | 5% (9% over $1M) | 4% "millionaire's surtax" on income over $1M (Ballot Measure 1, 2022) |

| Michigan | Flat | 4.05% | Rate fluctuates based on state revenue; 24 cities including Detroit (2.4%) levy city income taxes |

| Minnesota | Graduated | 5.35% – 9.85% | 4 brackets; among the highest top rates; top rate on income over $183,340 (single) |

| Mississippi | Flat | 4.7% | Transitioning to flat rate; phasing toward 4% by 2026 and eventually lower |

| Missouri | Graduated | 2% – 4.8% | Top rate reduced repeatedly; targeting 4.5% in future years |

| Montana | Graduated | 4.7% – 5.9% | Simplified to 2 brackets from 7 as of 2024 |

| Nebraska | Graduated | 2.46% – 5.2% | Top rate reducing annually toward 3.99% by 2027 |

| Nevada NO TAX | None | 0% | No income tax; gaming and hospitality revenues fund state |

| New Hampshire NO TAX | None | 0% | No wage income tax; interest/dividends tax fully phased out Jan 2025 |

| New Jersey | Graduated | 1.4% – 10.75% | 7 brackets; Kevin's state — $134.07 withheld this period. Also collects SUI/WF and FLI separately |

| New Mexico | Graduated | 1.7% – 5.9% | 4 brackets; top rate on income over $210,000 for single filers |

| New York | Graduated | 4% – 10.9% | 9 brackets; NYC residents pay additional city tax (3.078%–3.876%); Yonkers also levies local tax |

| North Carolina | Flat | 4.5% | Reducing toward 3.99% by 2026 under existing legislation |

| North Dakota | Graduated | 1.1% – 2.5% | Among the lowest state income tax rates in the country |

| Ohio | Graduated | 0% – 3.5% | No tax on income under ~$26,050; most municipalities impose local income taxes |

| Oklahoma | Graduated | 0.25% – 4.75% | 6 brackets; competitive rates for a non-zero-tax state |

| Oregon | Graduated | 4.75% – 9.9% | 4 brackets; no sales tax but among higher income tax states; Statewide Transit Tax also applies |

| Pennsylvania | Flat | 3.07% | Low flat rate; most municipalities impose local earned income tax; Philadelphia charges 3.75% for residents |

| Rhode Island | Graduated | 3.75% – 5.99% | 3 brackets; top rate on income over $176,050 |

| South Carolina | Graduated | 0% – 6.2% | Top rate reducing toward 6% by 2027; retirement income exclusions available |

| South Dakota NO TAX | None | 0% | No income tax; sales tax and tourism revenues fund state |

| Tennessee NO TAX | None | 0% | No income tax on wages since 2021; Hall Tax on dividends/interest was fully eliminated |

| Texas NO TAX | None | 0% | Constitutionally prohibited; highest property taxes partly offset the savings |

| Utah | Flat | 4.55% | Flat rate; credit for dependents available to reduce effective burden |

| Vermont | Graduated | 3.35% – 8.75% | 4 brackets; top rate on income over $213,150 for single filers |

| Virginia | Graduated | 2% – 5.75% | 4 brackets; notably the top rate of 5.75% kicks in at just $17,000 — meaning most workers pay the top rate |

| Washington NO TAX | None | 0% (wages) | No income tax on wages; capital gains tax of 7% applies to gains over $262,000 (not wages) |

| West Virginia | Graduated | 2.36% – 5.12% | Top rate reducing under phasedown legislation passed in 2023 |

| Wisconsin | Graduated | 3.54% – 7.65% | 4 brackets; top rate on income over $405,550 for single filers |

| Wyoming NO TAX | None | 0% | No income tax; mineral extraction revenues (coal, oil, gas) fund state government |

States with Additional Local Income Taxes

Beyond state-level taxes, several states allow cities and counties to impose their own local income taxes. These may appear as separate line items on your paystub.

| State / City | Local Tax Rate | Who Pays | Notes |

|---|---|---|---|

| New York City, NY | 3.078% – 3.876% | NYC residents | On top of NY state tax; among the highest combined state+local rates in the US |

| Yonkers, NY | 1.477% – 1.61% | Yonkers residents/non-residents | Surcharge on NY state liability |

| Maryland (all counties) | 2.25% – 3.2% | All MD residents | Every county and Baltimore City levies local income tax |

| Philadelphia, PA | 3.75% (residents) / 3.44% (non-residents) | Residents + workers in Philly | Applies even if you just work in Philadelphia but live elsewhere |

| Columbus / Cleveland, OH | 2.5% | Residents and workers | Most OH municipalities levy local income tax; rates vary by city |

| Indiana (all 92 counties) | 0.5% – 2.9% | All IN residents | County tax withheld based on county of residence; shown separately on paystubs |

| Detroit, MI | 2.4% (residents) / 1.2% (non-residents) | Residents + workers in Detroit | 24 Michigan cities total levy city income taxes |

| Louisville / Lexington, KY | 2.2% – 2.5% | Residents and workers | Called "Occupational Tax" or "Local Services Fee" in Kentucky |

| Alabama (Jefferson County) | 1% | Residents of Jefferson County | Occupational tax also levied by several AL cities |

| Oregon (Statewide Transit Tax) | 0.1% | All OR workers | Funds public transit; withheld separately from state income tax |

| San Francisco, CA | 0.38% – 0.76% | Employees and employers in SF | Payroll Expense Tax and Gross Receipts Tax; affects paystubs in some structures |

| Kansas City, MO | 1% | Residents and workers | Kansas City and St. Louis both levy city earnings taxes |

Other Deductions — Pre-Tax and Post-Tax Explained

Beyond statutory tax deductions, many paystubs include voluntary or employer-sponsored deductions for benefits and retirement plans. Kevin's paystub doesn't show these (he has no voluntary benefit deductions this period), but here is everything you might see on your own paystub.

Pre-Tax Deductions — Reduce Your Taxable Income

Pre-tax deductions are subtracted from gross pay before taxes are calculated. This reduces your taxable income, meaning you pay less in federal and state income tax. They do not, however, reduce FICA taxes (with some exceptions).

| Deduction | Common Label | Reduces Fed Tax? | Reduces FICA? | 2026 Limit |

|---|---|---|---|---|

| 401(k) Traditional | 401K, Ret, DCRET | Yes | No | $23,500 ($31,000 if age 50+) |

| 403(b) | 403B, TSA | Yes | No | $23,500 ($31,000 if age 50+) |

| Health Insurance Premium | MED, HLTH, INS | Yes | Yes (Section 125) | Varies by plan |

| Dental / Vision | DENT, VIS | Yes | Yes (Section 125) | Varies by plan |

| Health Savings Account (HSA) | HSA | Yes | Yes | $4,300 single / $8,550 family |

| Flexible Spending Account (FSA) | FSA, MED FSA | Yes | Yes | $3,300 (2026) |

| Dependent Care FSA | DCFSA, DEP CARE | Yes | Yes | $5,000 per household |

| Transit / Commuter Benefits | TRANSIT, COMMUTE | Yes | Yes | $325/month transit + $325/month parking |

| Life Insurance (over $50k) | GTL, GRP LIFE | Imputed income added | Yes on imputed | $50,000 threshold |

Post-Tax Deductions — No Tax Reduction Benefit

Post-tax deductions are taken from net pay after all taxes have been calculated and applied. They reduce your take-home pay but do not lower your tax burden.

| Deduction | Common Label | Why It's Post-Tax |

|---|---|---|

| Roth 401(k) | ROTH, ROTH 401K | Contributions taxed now; withdrawals in retirement are tax-free |

| After-Tax Life Insurance | LIFE, VOL LIFE | Voluntary supplemental life insurance above employer-provided coverage |

| Union Dues | UNION, DUES | Membership fees for labor unions |

| Wage Garnishments | GARN, LEVY | Court-ordered; child support, back taxes, student loans, creditor judgments |

| Charitable Contributions | CHARITY, UW | Payroll deduction for employer-sponsored giving programs |

| Employee Stock Purchase Plan | ESPP | After-tax contributions to purchase company stock at a discount |

Year-to-Date (YTD) Totals — Why This Column Is Critical

Every earnings and deduction line on a paystub has two columns: This Period and Year to Date (YTD). The YTD column is the running total from January 1 through the current pay date.

On Kevin's paystub (pay date March 24, 2026), his YTD figures tell a story about his year so far:

| Line Item | This Period | YTD Total | Implied Avg/Period |

|---|---|---|---|

| Gross Pay | $2,104.78 | $25,257.36 | ~$2,296/period |

| Federal Income Tax | $505.15 | $6,061.80 | $551/period |

| Social Security | $130.50 | $1,566.00 | $142/period |

| Medicare | $30.52 | $366.24 | $33/period |

| NJ State Tax | $134.07 | $1,608.84 | $146/period |

| NJ SUI/WF | $8.10 | $97.20 | $8.84/period |

| NJ FLI | $1.89 | $22.68 | $2.06/period |

| Total Deductions | $810.23 | $9,722.76 | $884/period |

| Net Pay | $1,294.55 | — | — |

Five ways to use YTD data

- Verify your W-2: Your December final paystub YTD gross should match Box 1 of your W-2 (adjusted for pre-tax deductions). If they don't match, contact payroll immediately.

- Track Social Security wage base: Once your YTD gross exceeds $176,100 (2026), Social Security withholding stops. Monitor this on your paystubs to anticipate the net pay increase.

- Confirm 401(k) contributions: The IRS limit for 401(k) contributions is $23,500 in 2026. Your YTD retirement deduction column helps ensure you don't inadvertently over-contribute.

- Income verification: Three months of paystubs with consistent YTD totals provide much stronger income proof to lenders than three paystubs with YTD figures that don't add up correctly.

- Spot payroll errors: If your YTD Social Security doesn't equal exactly 6.2% of your YTD gross (up to the wage base), something is wrong. Same check applies to Medicare at 1.45%.

Direct Deposit and the Payment Confirmation Section

The bottom strip of Kevin's paystub is the direct deposit advice section — a detachable record that confirms where the net pay was sent and serves as proof that the payment was made.

Key fields in the direct deposit section

- "THIS IS NOT A CHECK" — Required legal disclaimer. This document has no monetary value. The actual payment was transferred electronically. It cannot be cashed at a bank.

- Advice / Check Number (72728) — A unique transaction identifier. Matches the VCHR number at the top of the stub. Used for payroll reconciliation and to trace transactions.

- Account Number (xxxxxx1357) — The destination bank account, masked for security with only the last 4 digits visible.

- Transit / ABA — The bank routing number, also masked. Identifies the specific financial institution and branch.

- Amount ($1,294.55) — The exact net pay figure transferred. Must always match the Net Pay line on the stub.

Pay Frequency — Weekly, Bi-Weekly, Semi-Monthly, and Monthly Compared

Pay frequency determines how often you receive a paycheck and how your annual salary is divided across pay periods. Kevin is paid weekly — but there are four standard pay frequencies, each with different implications for cash flow, budgeting, and paystub reading.

| Frequency | Periods/Year | Annual Salary ÷ | Example (Kevin's ~$109K) | Common In |

|---|---|---|---|---|

| Weekly | 52 | ÷52 | ~$2,105/week | Construction, manufacturing, hourly workers |

| Bi-Weekly | 26 | ÷26 | ~$4,210/2 weeks | Most common in the US; ~43% of employers |

| Semi-Monthly | 24 | ÷24 | ~$4,560/half month | White-collar, professional services |

| Monthly | 12 | ÷12 | ~$9,121/month | Executive compensation, some international |

Bi-weekly vs. semi-monthly — the critical difference most people miss

These two are frequently confused. Bi-weekly means every two weeks — resulting in 26 paychecks per year. Semi-monthly means twice per month on fixed dates (typically the 1st and 15th) — resulting in exactly 24 paychecks per year. The distinction matters because:

- Bi-weekly employees receive two "extra" paychecks per year compared to semi-monthly (26 vs. 24)

- Two months per year, bi-weekly employees receive three paychecks in a single calendar month

- Semi-monthly paychecks are slightly larger per paycheck than bi-weekly at the same annual salary

- For hourly employees, bi-weekly is simpler since it always covers exactly two workweeks; semi-monthly can split a workweek across two pay periods

How to Spot Errors on Your Paystub — And What to Do

Payroll errors are more common than most people realize. Studies suggest that approximately 33% of employers make payroll errors in any given year, and the American Payroll Association estimates that payroll error rates for manual processes can run as high as 8%. Here's a systematic way to check your paystub for mistakes.

Self-Employed Paystubs — How to Create Your Own

Kevin's paystub is generated automatically by his employer's payroll system. If you're self-employed, freelancing, running a small business, or working as an independent contractor, you need to generate your own — and everything you see on Kevin's paystub is something you can produce for yourself accurately and professionally.

Is it legal to create your own paystub?

Yes — with one absolute condition. A paystub you create must accurately reflect income you actually earned. Creating a paystub to document real income for income verification purposes is entirely legal and is standard financial practice among self-employed individuals. Creating a paystub that misrepresents income is fraud — a federal crime.

What your self-employed paystub must show

The same fields as Kevin's: employer name and address (your business), employee name and address (you), pay period dates, gross pay, federal and state tax withholdings at the correct rates, FICA taxes at the self-employment rate, net pay, and YTD totals. There is no legal format requirement — but lenders and landlords expect a format that resembles what Kevin's looks like.

The self-employment tax difference on your paystub

The most common error self-employed workers make when creating paystubs is applying the wrong FICA rate. Kevin pays 6.2% Social Security and 1.45% Medicare because his employer pays the other half. As a self-employed worker, you pay both halves — 12.4% Social Security and 2.9% Medicare — for a total FICA burden of 15.3%. Your paystub must reflect the full self-employment rate to be consistent with your tax returns, which will show the full SE tax paid.

How to determine your gross pay as a self-employed worker

Your gross pay on a self-employed paystub is your gross revenue for the pay period — the total amount clients or customers paid you, before business expenses. Do not deduct business expenses from gross pay on your paystub. Business expenses reduce your taxable net income on Schedule C, not on your income documentation for lenders.

Handling irregular income

Freelance and gig income is often irregular — $3,000 one month, $8,500 the next. You have two legitimate approaches:

- Actual-period approach: Create a paystub for each period reflecting exactly what you earned. More accurate; may show variability.

- Monthly-average approach: Calculate your 3–6 month average and use that consistent figure. Smoother presentation; must still reflect actual total earnings.

Create a Self-Employed Paystub in Under 2 Minutes

PaystubASAP automatically applies the correct self-employment tax rates, state taxes for all 50 states, and YTD calculations — so your paystubs are accurate, professional, and consistent every time.

Generate My Paystub Now →Works for freelancers, 1099 contractors, gig workers & sole proprietors · Instant PDF download

Using Your Paystub for Income Verification

Paystubs are the primary income verification document accepted across virtually every financial context. Here's how to use them effectively for each major situation.

| Application Type | Paystubs Needed | Additional Docs | Key Fields Reviewed |

|---|---|---|---|

| Apartment Rental | 2–3 most recent | Bank statements | Gross monthly income ≥ 3× rent; YTD consistency |

| Car / Auto Loan | 2–3 most recent | Sometimes bank statements | Gross monthly income; employment stability |

| Personal Loan | 2–3 most recent | Bank statements | Gross income; net pay (ability to service debt) |

| Mortgage | 2–3 most recent | 2 years tax returns, W-2s, bank statements | All fields; 2-year income history; YTD vs. prior year |

| Credit Card | 1–2 most recent | Sometimes none | Annual gross income; employment status |

| Government Benefits | Varies by program | Tax returns, ID | Net income; benefit deductions |

| Child Support Filing | 3–6 most recent | Tax returns | Gross income; overtime; bonus patterns |

| SBA / Business Loan | 3–6 most recent | Business tax returns, P&L | Business income stability; owner compensation |

Complete Paystub Glossary — 40+ Terms Defined

Every term you might encounter on a paystub, defined in plain English.

Frequently Asked Questions About Paystubs

The gap between gross and net pay is entirely normal and reflects the combined burden of federal income tax, FICA (Social Security and Medicare), state income tax, and any voluntary benefit deductions. For a single filer earning a median US wage, the total deduction rate typically runs 25–35% of gross pay. Higher earners in high-tax states like California or New York can see 40–45% of their gross disappear before their paycheck arrives. The money isn't "lost" — federal and state taxes fund public services, FICA funds your future Social Security and Medicare benefits, and pre-tax deductions like 401(k) contributions are going into your own retirement account.

Bi-weekly means every two weeks — 26 paychecks per year. Semi-monthly means twice per month on fixed dates (usually the 1st and 15th) — 24 paychecks per year. The difference matters because bi-weekly employees receive two "extra" paychecks annually compared to semi-monthly employees — but each bi-weekly check is slightly smaller than a semi-monthly check at the same annual salary. Twice per year, bi-weekly employees receive three paychecks in a single month.

Federal withholding is based on your W-4 elections — filing status and any additional withholding or deductions you specified. If you claimed too few allowances or forgot to account for a second job, you may be over-withheld. If you claimed too many or have significant deductions not reflected on your W-4, you may be under-withheld. The IRS Withholding Estimator at IRS.gov can help you calculate the correct W-4 settings. You can submit a new W-4 to your employer at any time — there's no limit to how often you can update it.

The most likely explanation is that your YTD gross pay crossed the Social Security wage base ($176,100 in 2026). Once you've paid Social Security tax on $176,100 of earnings, no further Social Security (6.2%) is withheld for the rest of the year — a jump of $128 more per week for an employee at Kevin's income level. Other possible reasons: a pre-tax deduction was maxed out (like 401k contributions hitting the $23,500 limit), a benefit plan year ended, or your employer corrected an over-withholding error from earlier in the year.

The general guidance from financial advisors is to keep paystubs for one year — until you've filed your tax return and verified your W-2 matches your final paystub's YTD figures. After that verification, you can safely discard the interim paystubs and keep only the final one from December. However, keep paystubs longer in certain situations: if you're involved in a wage dispute or lawsuit, if you're applying for a mortgage or other major loan, if you're self-employed and paystubs are part of your income documentation package, or if you claimed unusual deductions on your tax return that might be audited.

Yes — and they should. Creating a paystub that accurately documents your real self-employment income is entirely legal and is the standard approach for freelancers, independent contractors, gig economy workers, and small business owners who need proof of income. The key word is accurately — every figure on a self-employed paystub must reflect actual earnings. Using a paystub generator to document real income is legitimate; using one to misrepresent income you didn't earn is fraud. PaystubASAP is designed specifically for this use case, with automatic self-employment tax rates, all 50 states covered, and YTD calculations that keep multiple stubs consistent.

Several situations can cause this. First, check whether you work in a different state than you live in — if you commute to a state with income tax even though you live in a no-tax state, you may owe tax to the work state (though some states have reciprocity agreements). Second, some states (like Washington) have no income tax on wages but do have other payroll taxes like the Washington Cares Fund long-term care tax. Third, if you recently moved to a no-tax state, your employer may not have updated your state on file yet — contact HR to update your address. Fourth, some employers withhold taxes for the state where their headquarters is located if they haven't properly set up multi-state payroll.

"NON-NEGOTIABLE" printed on a paystub (as on Kevin's — "NON-NEGOTIABLE — AUTO DEPOSIT") means the document is not a negotiable instrument — it cannot be endorsed and cashed at a bank like a paper check. It is purely an informational record of a payment that was made electronically via direct deposit. This disclaimer is required on direct deposit advice slips to distinguish them from actual checks. If you receive a paper check instead of a direct deposit, the check itself is a negotiable instrument, but the paystub attached to it is still non-negotiable.

A paystub is issued every pay period and shows earnings and withholdings for that specific period, plus YTD totals. A W-2 is issued annually (by January 31) and summarizes your entire year's earnings and withholdings for IRS tax filing purposes. Your final December paystub's YTD figures should closely match your W-2 — with some differences because W-2 wages in Box 1 exclude pre-tax deductions (401k, health insurance, FSA/HSA) that your gross pay includes. The W-2 is the official tax document; the paystub is the periodic detail behind it.

Payroll withholding is an estimate of your annual tax liability, not a precise calculation. You may owe taxes at filing if: you have multiple income sources (two jobs, freelance work, investment income) and each employer's withholding only accounts for that one income stream; you claimed too many allowances on your W-4; you received a large bonus or commission that wasn't withheld at a high enough rate; or you had income from sources with no withholding (rental income, self-employment, cryptocurrency gains). To avoid owing in future years, adjust your W-4 with your employer or make quarterly estimated tax payments for non-employment income.

The Bottom Line

A paystub is not a confusing bureaucratic document — it's a transparent record of one of the most important financial transactions in your life. Every line has a meaning, every number has a formula, and every field tells you something specific about your earnings, your taxes, and your financial standing.

Whether you're reading your own paystub to understand where your money goes, checking it for errors that cost you money, using it to apply for a loan or apartment, or creating one as a self-employed worker to document your income — this guide has given you everything you need to do it with complete confidence.

Bookmark this page. Share it with a friend who's confused about their paystub. And if you need to generate a professional paystub — whether you're an employer, an employee, or self-employed — PaystubASAP has you covered in under two minutes.

Generate a Professional Paystub in Under 2 Minutes

PaystubASAP produces accurate, professional paystubs for every situation — employers paying staff, self-employed workers documenting income, freelancers applying for loans, and gig workers proving earnings. Every field from this guide, automatically calculated and formatted.

Create My Paystub Now →100% accurate 2026 tax calculations for all 50 states · Instant PDF · Works for W-2 & 1099